Kodak Gets Messy

*cracks knuckles*

Eastman Kodak’s (KODK) Q2’25 Earnings disclosure caused quite a stir recently but it’s by far not the first time or the most dramatic report on the manufacturer.

As usual with any drama, there’s misinformation, misunderstanding, miscommunication…

Especially when folks with no corporate/finance knowledge or experience interpret specific accounting disclosures or financial statements. (Anybody who worked (s) in public audit or technical accounting or SEC financial reporting in the crowd today? Just me?)

So what happened this time?

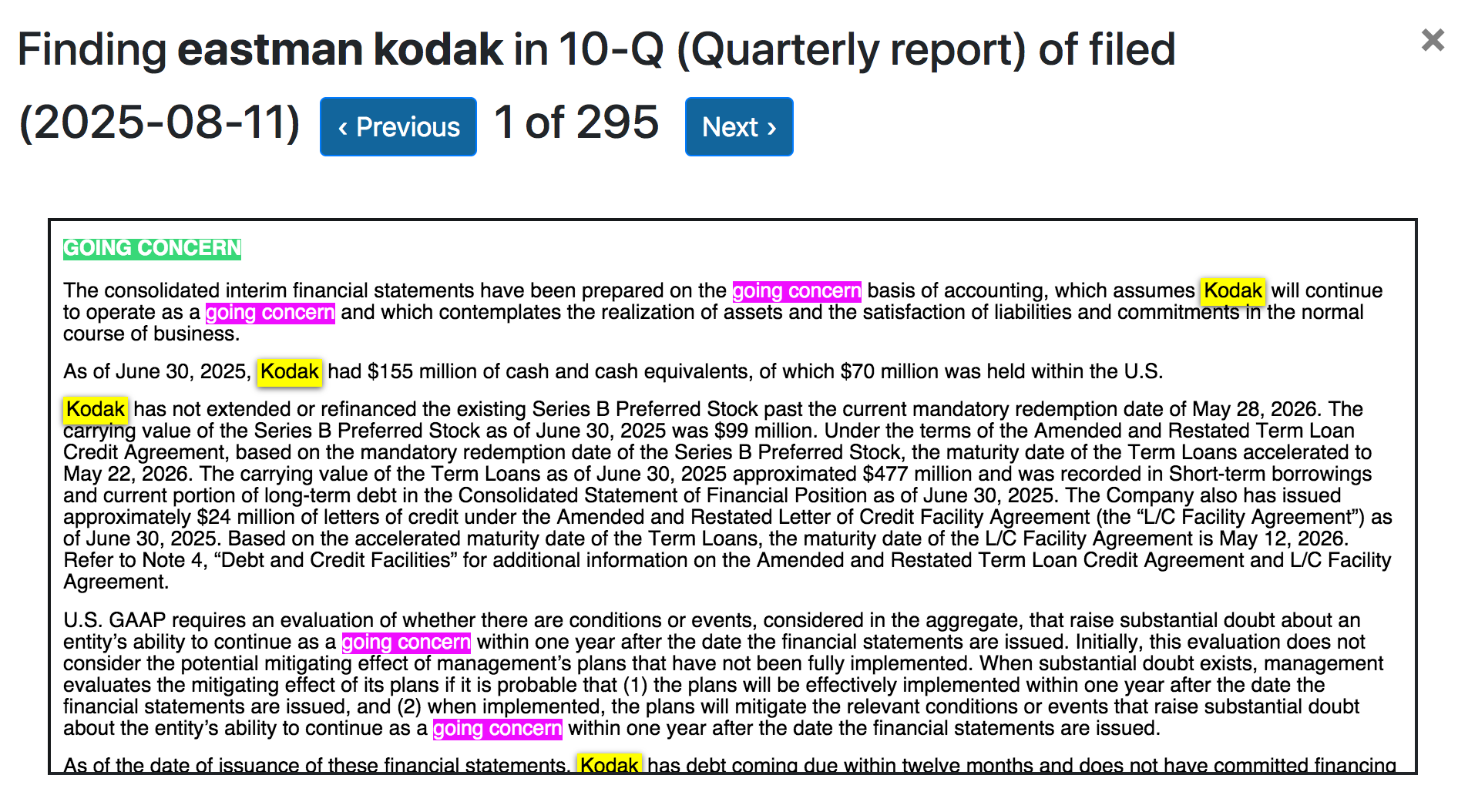

Well, alongside their poor Q2’25 earnings release, EASTMAN Kodak was required to disclose substantial doubt about meeting their debt obligations due in the next year.

Aka a going concern disclosure required by financial reporting rules.

I’ve heard some say it’s a big deal, others say it’s exaggerated, others with large followings get facts completely wrong.

BTW - Eastman Kodak is not Kodak Alaris. Eastman Kodak is the manufacturer of film at Eastman Business Park in Rochester, NY. Alaris might “market”/“sell” the consumer film but Eastman makes it and they also still make/sell the motion picture film. So no Eastman, no film.

For the purposes of getting this out of my head, because I’ve hyperfixated on Kodak research now including reading most of their Q2’25 10Q and Q4’24 10K for funzies and I’m not letting THAT be for nothing, here’s a post containing some, not all, of my current thoughts.

First of all, there is A LOT going on with Kodak.

And it’s messy.

And I can’t possibly conjure the amount of energy it would take to talk about it all so I’ll try to keep this short for both you and me.

Going Concern Concept & Disclosure

The first and primary point I want to briefly touch on is the "going concern disclosure” from Kodak in their Q2’25 earnings release.

In the most basic terms, a going concern is an assumption that a business has the ability to continue operating in the near future, technically the proceeding 12 months.

If you want to do your due diligence and read all of their reports, you can visit sec.gov/edgar and type in Kodak’s ticker or their name to find all of their publicly filed reporting to the SEC:

https://www.sec.gov/edgar/search/

This will give you much better information because Kodak didn’t release the full SEC reports in their press release page. The PDF attachments they include are NOT what is filed with the SEC and are bare bones compared to what’s available on the Edgar system.

What I saw triggering this going-concern disclosure from Kodak is an acceleration of the due date of their Term Loan Agreement, a substantial debt. The acceleration was triggered by a technical aspect of one of their equity instruments, the Series B.

Now both have large amounts due in 2026, less than 12 months from their Q2’25 10Q.

Kodak doesn’t have the guaranteed funds/liquidity at the moment to pay that.

And that’s why they are required to issue a going-concern disclosure.

I know their PR machine published a statement after a bunch of quite dramatic articles came out about this. The statement was meant to assuage public concern.

But it’s not not nothing.

It’s actually a bit serious.

And don’t let them put you off.

It’s not just a “required technical disclosure thing from the silly accountants who are just being really picky and it’s nothing to worry about, nothing to see here” (I’m paraphrasing)

It means that Kodak is in a poor working capital position. They have large short term liabilities and no guaranteed solution to pay off those liabilities at the time of the earnings report.

Of course, large companies play with debt and equity leveraging and financing all the time. They twist and tie themselves up in knots with various complicated agreements and financial instruments. They have teams and outside consultants dedicated to this. They redo things all the time in large amounts. It’s totally wild. And unless the lendors see serious doubt of the eventual ability to pay it back or they breach any conditions of the agreement, they continue the process. Or they find another lendor or investor to refinance with.

I have no doubt Kodak will manage to complete the work-arounds on this and they already have plans in the works.

So no, they aren’t going anywhere. For now.

What I do find a bit unnerving is the heavy amount of debt and equity financing and activity they have alongside thinner margins, decreasing revenues and sales volume in their primary revenue stream, investment setbacks and competition issues, rising supply chain costs, litigation, failed government project loans due to suspected insider trading and sketchy management, and so on.

Some of those things are more recent than others.

They recently recorded a $17m impairment in their $25m investment into Wildcat, which they had invested in to get into the battery? industry by leveraging their coating technologies. That’s one more yellow flag on top of a mountain in their history.

My personal favorite is the 2020 situation with the federal loan that could have launched them into the healthcare pharma manufacturing industry even though they didn’t really have pharmaceutical experience, but instead HR/Legal/management did some sketchy stuff with stock options, a board member funnelled stock into a charity, two other people in the deal were arrested for insider trading, and the deal never materialized. And management got off (supposedly) on a PR technicality and slapped on the wrist for having poor internal controls and an overwhelmed general counsel?

Basically sketchy management combined with deficiencies in internal controls (essentially checks and balances) is a major red flag.

Kodak and Film

Kodak doesn’t see film as big business growth potential in their future.

Their old boy old world greedy beady little eyes see pharmaceuticals. Chemicals manufacturing. This reporting segment (Advanced Materials and Chemicals) of Kodak is actually offsetting their Print segment downturns. So is their Brand segment which is brand licensing, this was up in 2025 from 2024.

Medical/chemical/materials tech is probably one of the best ways to turn the company to remotely thrive again someday.

They’ve made small investments into the film production facilities but this is mainly to catch up with the increasing demand and revenue they didn’t see coming back.

They are making bigger investments in other areas in a more proactive sense to enter new markets.

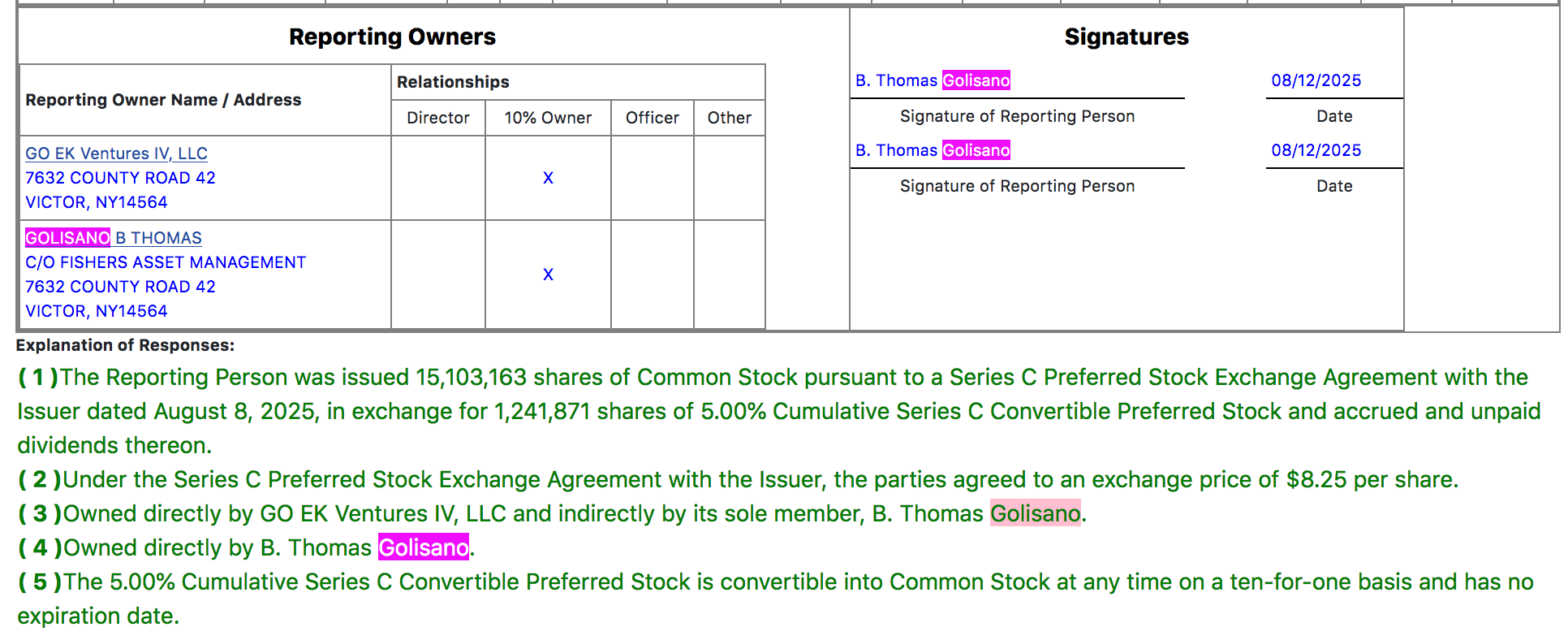

And B. Thomas Golisano has increasingly bet on them in multiple ways from multiple companies/angles, especially very recently.

Investments and future strategy - Excerpts from their Q2’25 10Q:

“Kodak has utilized an existing production coating facility to manufacture coated substrates for EV cell assembly. Kodak is evaluating expansion or enhancement of this facility to serve a wider variety of production level customers.”

“Reagent Manufacturing - Kodak plans to capitalize on its existing chemical manufacturing expertise, including current production of unregulated Key Starting Materials for pharmaceutical products, to implement an expansion into manufacturing Diagnostic Test Reagent solutions. Kodak has started construction of a Current Good Manufacturing Practice ("cGMP") lab and manufacturing facility to manufacture reagents for healthcare applications within an existing building located at EBP. Production is scheduled to begin by the end of 2025.”

“Light-Blocking Technology - A proprietary technology initially developed for electrophotographic toners is being leveraged to commercialize a carbon-less fabric coating designed to offer superior light management, from complete blackout to selective light filtering, and coating compatibility with an unmatched range of fabrics and also to manage ultraviolet and/or infrared light in addition to visible light. Kodak has installed a production-scale machine to coat fabrics in EBP, located in Rochester, NY and continues to explore strategic alternatives in order to commercialize this technology.”

“Transparent Antennas - Kodak plans to leverage its proprietary copper micro-wire technologies and high-resolution printing expertise to contract-manufacture custom transparent antennas for automotive, commercial construction, and other applications requiring excellent radio frequency (“RF”) and optical performance. The integration of antennas is growing worldwide due to the rapid expansion of 5G and an overall increase in RF communications, and the ubiquity of glass surfaces makes transparent antennas attractive for multiple end-use markets. Kodak is evaluating this unique printing technology and expertise for transparent heaters to be used in biomedical analytical devices and telecom applications such as satellite dishes.”

“The Company remains interested in working with governmental agencies to leverage its assets and technology to on-shore manufacturing of pharmaceutical and other healthcare materials.”

“Kodak plans to capitalize on its intellectual property through new business or licensing opportunities in 3D printing materials, smart material applications, and printed electronics markets.”

Conclusion

And this is just a tiny glimpse of the story.

Kodak has a lot to leverage and even if eventually they manage themselves to another bankruptcy, that’s not a true end game situation either.

So, do your own research, read the company’s SEC reports if you want to dive into how they are doing in detail, although that’s certainly not the whole picture by a thousand miles.

I don’t think Kodak is going anywhere anytime soon, however I wouldn’t say there’s nothing concerning in recent developments.

Certainly don’t buy their PR machine without validating their claims including their creative use of the phrase “virtually net debt free”. LOL

They will continue to have debt even if their plans succeed and likely always will. Large term loans and LOC (letters of credit) are common business tools to finance large scale operations, investments, or refinance older debt and other activities. However, with big debt comes big interest payments. Usually paid in cash, but now Kodak is paying them PIK, which means payment-in-kind. Interesting…

Anyways, that’s enough for me today!

I’ll leave you with a reminder to also support OTHER film companies making color film because relying too much on one source for anything is always a risk. Especially when that source is a publicly traded american manufacturing corporation riddled with issues and history that could take as much time to read through as 10 rolls of film shot on a half frame camera takes to scan on an Epson v600.

K luv u, byeee.

~M

Thank you for the informative analysis and clarity on the Kodak news at last - perhaps because you’re more interested in the reality than in getting eyeballs 👀/engagement stats. 🙏

Great stuff—thanks for adding some facts to the discussion. There are too many people out there feeding the echo chamber of misinformation. I’ve been hoping that someone who actually understands business and financial reporting would tackle this story, as you have done. Many thanks!